Taxes are one of the most significant places a steward can get more intentional. Most people just accept whatever their employer withholds and move on. Understanding how taxes work means you can legally direct more money toward giving and investing rather than handing it blindly to a government that’ll spend it for you.

The US tax code is one of the most complicated pieces of literature ever written, so let’s start in familiar territory and then dive deep.

First, we go back to our cast of characters. The farmer, the quilter, the shepherd, the mason, and the lumberjack are all busy focusing on what they do best and then trading that value with each other. Eventually they decide that sharing some common things like schools, roads, and fire protection would be worth chipping in part of their money for. This pooled money allows some people to rule, protect, and educate the entire group.

Zoom to our modern world and taxes are dizzying. You have federal tax, state tax, payroll tax, capital gains tax, property tax, sales tax, estate tax, and not to mention silent taxes we pay like inflation and tariffs! Every level of government dips their hands in our wallets. It feels violating, but I would rather focus on the parts I have some control over. If you are upset about how much you get taxed in the US, look anywhere else in the world and you’ll see we pay less (whether we get more out of our tax dollars than other countries is another topic).

From a stewardship perspective, I certainly don’t agree with all the ways the government spends our tax money (wars), but taxes are an inevitable reality of life. Jesus tells us to give to Caesar what is Caesar’s and give to God what is God’s. I wish he taught us that it was our moral duty to evade all taxes so that we’d have more to keep and manage, but alas. Jesus taught his disciples to pay their dues to the then-ruling Roman Empire.

To avoid taxes entirely you’d have to make no money, own nothing, buy nothing, pass on nothing, or do a lot of sketchy stuff and risk jail. I would rather understand how taxes work and find smart, legal ways to reduce them so that I can make stewardship decisions instead of the government. If I am paying taxes that means I am making money, so any exercise in reducing taxes should start by recognizing the privileged position it is to be in.

Key Takeaways

This post gets technical fast. If you’re just getting started, read these main ideas and skim the rest — come back when the details start to matter.

-

The income you get taxed on is much lower than what you actually earn because of deductions, retirement account contributions, and other adjustments. Much of this long post breaks down ways to increase the gap between what you make and what you get taxed on.

-

Tax brackets are progressive buckets, not blanket rates. Everyone starts out in the lowest tax bracket and additional income bumps into higher buckets as it exceeds certain thresholds. The effective rate you pay (the overall %) is always lower than the top bracket your income lands in.

-

Tax-advantaged accounts (HSA, 401k, Traditional IRA) are great tools and directly reduce what you owe in taxes now. For most employees, this is the single highest-leverage move. Note that this money is difficult (not impossible) to access without penalty before retirement age.

-

Business owners pay far less tax because the tax code heavily favors business ownership. Even for the self-employed and freelancers, there are simple structures that can significantly reduce your tax burden.

-

Sometimes paying taxes now is smarter. Tax-advantaged accounts skip taxes now and defer them to an unknown future. Depending on your income situation and future tax rate policy, taxes could be meaningfully higher in the future. Roth accounts and taxable brokerages are good places to invest extra dollars that shouldn’t just blindly be thrown into tax-advantaged accounts.

Hiring an Accountant

Folks with simple tax situations like a single W-2 can likely file their taxes themselves with the help of software. For everyone else, an accountant is well worth the cost for their expertise, ability to help navigate your specific situation, and deep knowledge of tax saving strategies. As a stubborn DIYer I find hiring an accountant one of the best possible uses of time and money. I have no fancy letters to my name so all of this is just personal experience to take at your own risk. Go hire someone with those fancy letters that keep up to date with the latest tax code changes.

Types of Tax

Federal tax - This includes income tax, a percentage of your income that goes to the federal government based on how much you make, as well as payroll taxes which are payments into the social security, Medicare, and unemployment systems.

State tax - each state has different rules. Some have no state income tax, some use a flat percentage, and others use a progressive (graduated-rate) system. This money goes to fund schools, highways, and all other things states pay for.

Property tax - local governments assign a value to physical property like homes, land, and cars; then apply a fixed percentage tax against that value. The tax value is often (lower) than the market value you might buy or sell something for.

Capital gains tax - When you sell an asset that has grown in value from the price you bought it at, you generate capital gains. Things like home sales and investments in taxable accounts sold for more than the purchase price. Capital gains are based on when you sell a position and depend on how long you held it - short term (less than a year) and long term (over a year). Short term gains get taxed like income, long term capital gains get taxed in lower brackets than income.

Sales tax - states decide on a flat percentage applied when you buy things like groceries, coffee, gas, etc. States with no income tax usually “get it back” with higher sales and property taxes than states with income tax.

Estate tax - Taxes on the value of a dead person’s assets typically paid out of the estate before transferring to the heirs.

Important numbers that impact the tax you pay

Total Income

The starting point for everything that follows, but not used for much beyond anchoring on for personal knowledge or by landlords and lenders deciding how likely you are to pay them.

To calculate: Total of all income from different sources: wages, bonuses, interest, dividends, capital gains, rental income, and a whole long list that includes jury duty and Olympic medals. This includes forms like W-2, 1099, K-1, 1099-INT, 1099-DIV, and more.

Adjusted Gross Income (AGI)

The starting point for taxable income, also influences things like income-driven student loan payments, qualification for college tuition financial aid, deductibility of medical expenses, charity deductions, and more.

To calculate: Total Income minus “above-the-line” deductions like contributions to pre-tax accounts (HSA, 401k, Trad IRA), qualified business expenses, half of self-employment taxes, self-employed health insurance deductions, and many more items worth researching relevant to your specific situation.

Modified Adjusted Gross Income (MAGI)

Comprehensive picture of disposable income that determines eligibility for things like healthcare premium subsidies, student loan deductions, Roth/Traditional IRA contributions, child tax credits, adoption tax credits, and education-related tax credits.

MAGI is critical for determining subsidies (discounts) to monthly health insurance premiums under the Affordable Care Act (ACA), often with precise thresholds that can result in thousands of dollars of difference in premiums.

To calculate: For many, AGI will be the same as MAGI and the difference won’t matter a lot. MAGI definitions can change depending on the specific tax benefit in question, but generally it involves adding back certain deductions and exclusions to AGI.

Taxable Income

The final number that gets run through tax brackets to arrive at the federal and state taxes you owe each year.

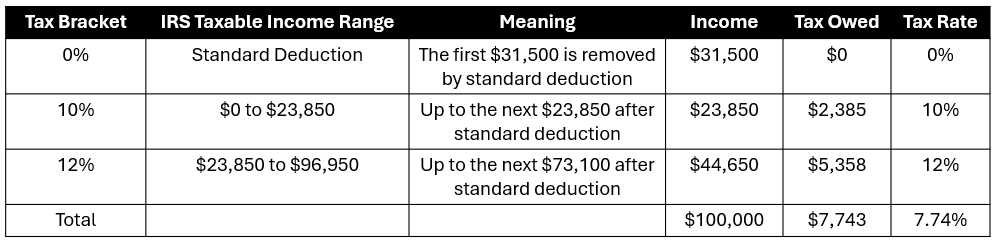

To calculate: Start with AGI, then subtract either whichever number is bigger between the standard deduction and itemized deductions. Most people take the standard deduction, a flat number each year based on your filing situation (individual, married filing jointly, etc.). Next we’ll talk about the many ways to lower taxable income.

Tax Brackets

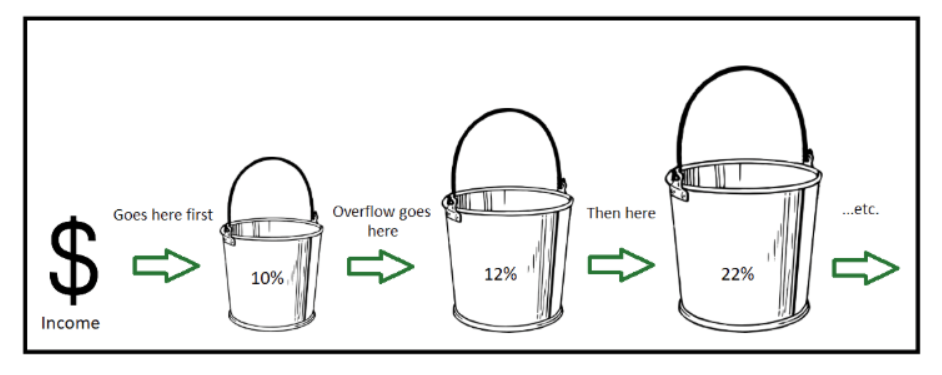

Taxable income flows through progressive tax brackets that rise along with income. The dollar amount it takes to “fill up” each tax bracket depends on the amounts set by the IRS each year on your tax filing status (individual, married filing jointly (MFJ), etc.). Imagine taxable income filling up tax brackets like buckets, starting with the lowest tax buckets and spilling into higher ones until there is no more taxable income to fill further. Nobody pays the highest percentage on every dollar of taxable income, so your total effective tax rate will be lower than the highest tax bracket you hit.

Let’s run through an example of a couple with $100k in taxable income, married-filing-jointly in 2025 and taking the standard deduction of $31,500 leaving them with $68,500 to run through the 2025 IRS progressive federal tax brackets.

State taxes typically start with the same federal taxable income, then apply either a flat percent, a progressive tax structure, or no state tax at all.

On your personal tax return, you or your accountant will calculate the total federal and state taxes owed, compare to what you have already paid in that tax year, and you will either owe taxes or be paid back for over-withholding.

Reducing Taxes for employees (W-2)

As an employee, your paycheck gets hit with federal, state, and payroll tax. Employees and employers split the 15.3% payroll tax and pay 7.65% each even though you never see the employer side on the W-2.

Reduce AGI and thus taxable income by contributing to tax advantaged accounts. Accounts like HSAs and FSAs can be completely tax-free when used properly. 401ks and Traditional IRAs can defer income taxes by avoiding them now and paying them later when you withdraw. Roth IRAs and 529 are still tax advantaged but the other way around from 401k/Trad IRA - they require you to pay income tax now, but down the road when you withdraw they are tax free. Whether you pay taxes now or later depends largely on the tax bracket you are in now versus what you think you’ll be in later. If you’re in a high earning, high tax bracket now you may be better off deferring taxes to later in life when you would withdraw at a lower income, lower tax bracket. While you may expect to live on a lower income later, you cannot predict tax brackets in the future. Accounts like Roth IRAs and 529s provide a nice hedge against potential future tax increases by paying tax now and then withdrawing tax free.

See Account Types for a full breakdown of each account type, contribution limits, and how to prioritize them.

Other ways to reduce taxable income include tax loss harvesting and itemizing deductions that would add together to exceed the standard deduction, like the total of charitable contributions, mortgage interest, state and local taxes (SALT), property taxes (home, vehicle), and medical/dental expenses that exceed 7.5% of AGI.

Reducing taxes for the self-employed, freelancers, and business owners

All the options available to employees exist to this crowd as well, but this group has some extra special benefits available to them. If you see the tax code as being written by rich people for rich people and see that rich people often run businesses, you will see clearly how the tax system is rigged to favor business ownership.

If you are paid as a 1099 contractor, you get slammed at tax time because you pay income and payroll taxes from both the employee side like a W-2, but also the employer side of payroll taxes (an additional 7.65%, unlike in a W-2). The good news is you are already getting taxed like a business and thus can reduce your final taxable income by taking off:

• Expenses to run the business: materials, computers, Wi-Fi, cell phone, software subscriptions, etc.

• Qualified Business Income (QBI) deduction aka 199A Deduction: 20% of K1

• Self-employed health insurance deductions

• Employer-side 401k and HSA contributions (if eligible)

• Business travel: flights, hotels, rental car

• Business mileage on your own car: track mileage, possibly buy a car for business use

• 50% of business meals

• Home office deduction

• Self-employment tax deduction for 1099 - half of payroll tax (7.65% of 1099 amount)

• Depreciation of assets

There’s no sense in spending money just for a business tax write-off. It is about shifting legitimate business expenses away from your personal accounts and onto your business ones. Wi-Fi may cost $100 either way, but paid for as a business expense it takes just $100 of business income to cover it, while paid for on a personal account it would take $130-$135 of income to pay the same $100 after taxes.

These deductions give a huge advantage to business owners, but the real leverage comes from passing 1099 income through the right business structure. Options include Sole Proprietorship, Single-Member LLC, and what I will focus on most: LLC with an S election which gives you S-Corp tax treatment for an LLC.

If you qualify for this LLC with S election structure, you can split income into salary and distributions to significantly reduce your total tax bill. You can pay yourself a reasonable W-2 salary for your industry per IRS guidelines, then the rest in K-1 ownership distributions that are as easy as writing a check to yourself from your business. Both W-2 and K-1 get hit with federal and state income tax, but the K-1 distributions do not get hit with the 15.3% payroll tax. If you target a 40% W-2 and 60% K-1 split of business income, that’s an immediate 9% (60% K1 * 15.3% payroll tax) tax savings compared to it all being 1099 income. Layer in 20% Qualified Business Income (QBI) deductions off K-1 income and that’s another 12% tax savings (60% K1 * 20% QBI). Together these two save you 21% of your income from taxes, all through legal paths in the tax code.

Owning a business gives you a ton of nice tax advantages. While it is more involved to run a business than perform the same tasks as a W-2 employee, you can often be paid more for the exact same work since the company does not have to pay for extra things like payroll taxes, health insurance, and all the other benefits companies provide to their employees. There is a lot more risk in owning a business - no paid time off, no steady predictable monthly paycheck - but for many the risk/reward is worth it in addition to all the opportunities to lower your tax bill.

When to pay more in taxes

Tax-advantaged accounts are great, but they come with the tradeoff that they make money difficult (not impossible) to access without penalty before retirement age. It is possible to charge hard in the direction of tax optimization and build a sizeable 401k, but not feel any financial flexibility from this “locked up” money. Choosing to pay taxes at current rates and use after-tax accounts may be worth it for the flexibility alone.

Deferring taxes is a bet that your future tax bracket will be lower than what it is now. If you’re making a huge income and are hitting the higher tax brackets, it is reasonable to defer taxes and bet that in the future your income or withdrawals would be in a lower tax bracket. You may find your taxable income all stays in the lower tax buckets and make the choice to “fill up” the space remaining in lower tax buckets with a few moves that on paper increase your taxable income (e.g.: Roth conversions, harvest capital gains, etc.)

In this scenario you are betting that in the future the lowest tax brackets will be higher than 12%, which is likely a great bet. You pay a little more taxes now than you would if you deferred, but money that goes into Roth accounts grows tax free for the rest of your life, and money in a brokerage account is accessible to you anytime, not locked up until you are in retirement age.

How rich people avoid taxes

The cry on the street is to tax the rich because the system is not fair and they should pay their part. It is both true that rich people pay a huge portion of the total taxes the government takes in, AND it is bananas that a tech CEO could make in minutes what a working person might make in their entire lifetime. The system was designed by and for the benefit of the rich, but the income tax brackets we talked about apply to everyone, so how do rich people get by paying so little in taxes?

Notice most taxes we pay come through some sort of paycheck (income and payroll taxes). Rich people go to great lengths to access cash flow without earning lots of income. They do this by owning things - businesses, real estate, fancy art, you name it - things that grow in value on paper (equity) but don’t actually get taxed until they are sold.

When assets are sold, they are typically taxed at capital gains rates, which are meaningfully lower than taxes on income. This is huge for normal people too - below a certain taxable income threshold, long-term capital gains could be taxed at 0% (state taxes still apply).

Think of Steve Jobs famously taking a $1 salary. He paid no income taxes on that, but he got paid in Apple stock. When that stock exploded in value, on paper he had an enormous amount of money but wouldn’t owe tax until he sold stock. If he needed money he could even get a loan against the equity he had in his Apple stock, giving him cash to spend without triggering a taxable sale.

Rich people use business structures, real estate, and other assets to gain equity, keep income low on paper, deduct everything they can, and find every fancy way to engineer the lowest possible tax bill.

If you tax the rich too much they can just move to another country and take their money and job-creating businesses with them! So the rules benefit the rich and prevent the system from swinging away from their favor. Many of these rules are available to ordinary people - knowing how the system works and how business structure can help is enough to pay less taxes and move on with life.

Conclusion

To pay less taxes you can: earn less money, contribute to retirement accounts, move to a lower tax state, give to charity, get married, have children, have a mortgage, start a business, invest in real estate, or lose money in investments. Of course not all of those will save you money overall, but they will cut down your tax bill.

Will tax brackets go up in the future? I don’t know, but I can’t see a future United States without higher taxes somewhere. I like saving on taxes now even if I pay them later (401ks), but I’m also willing to give up perfect tax efficiency to hedge against future increases, which is why I also use the Roth IRA.

Either way I think the point is to understand the system well enough to make intentional decisions about where money goes. The difference between blindly handing over more than you owe and thoughtfully directing those dollars is real stewardship.